✖

U.S. Car Rental Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Leisure and Tourism, Business and Corporate), vehicle type, rental duration, service model, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

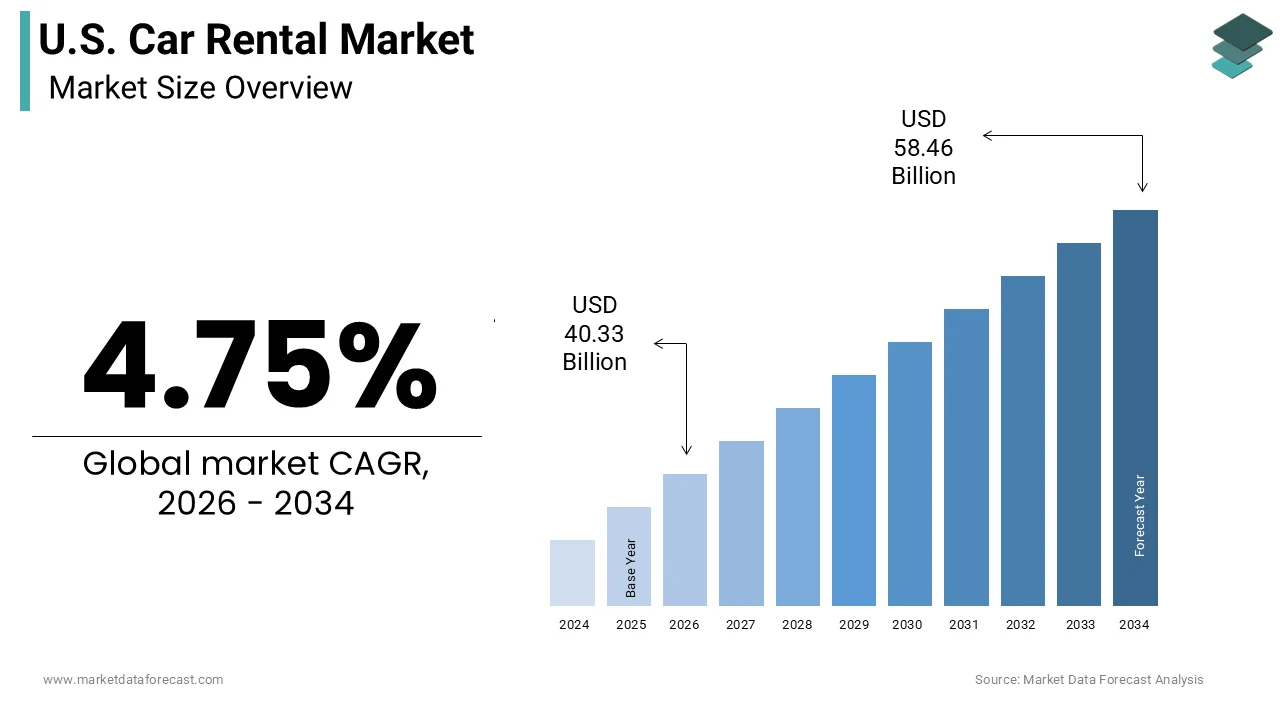

The U.S. car rental market size was calculated to be USD 38.50 billion in 2025 and is anticipated to be worth USD 58.46 billion by 2034, from USD 40.33 billion in 2026, growing at a CAGR of 4.75% during the forecast period.

The United States is projected to maintain a strong market position through 2030 due to its advanced transportation infrastructure and a deeply ingrained car-centric culture. The U.S. car rental market constitutes a dynamic sector within the broader transportation and hospitality industry, characterized by the short-term leasing of vehicles to consumers for personal or business use. This industry serves as a critical infrastructure component, facilitating mobility for tourists, business travelers, and individuals requiring temporary vehicle access due to maintenance or specific logistical needs. The operational landscape is defined by a mix of traditional brick-and-mortar locations at airports and city centers, alongside an increasingly dominant digital presence that enables seamless booking and keyless entry experiences. According to the United States Census Bureau, approximately 91.7% of American households have at least one vehicle available, creating a vast potential customer base for rental services when primary vehicles are unavailable. As per the Federal Highway Administration, the total number of vehicle miles traveled in the U.S. reached approximately 3.2 trillion miles in recent years, underscoring the heavy reliance on personal mobility. Furthermore, the Bureau of Transportation Statistics indicates that domestic air passenger traffic has recovered significantly, with over 900 million enplanements recorded annually, which directly correlates to heightened demand for airport-based rental services. The industry is also influenced by shifting consumer preferences toward experiential travel, with the US Travel Association noting that leisure travel spending has surpassed pre-pandemic levels. These foundational metrics illustrate a robust ecosystem where vehicle availability, convenience, and technological integration define the competitive environment for major operators and emerging digital platforms alike.

The resurgence and sustained growth of domestic leisure travel is driving the growth of the U.S. car rental market. As international travel complexities persist or fluctuate, American consumers have increasingly turned to intra-country destinations, necessitating reliable personal transportation for exploration and convenience. According to the US Travel Association, domestic leisure travel spending reached $841 Billion in 2023, which is demonstrating robust recovery and exceeding levels observed in 2019. According to the National Park Service, over 325 million recreation visits to national parks in a single recent year, a statistic that highlights the preference for road trips and destinations that are often inaccessible via public transit. This trend is further amplified by the rise of experiential tourism, where visitors seek to explore rural areas, small towns, and scenic byways. According to the American Automobile Association, 82% of travelers planned a road trip in 2024, reinforcing the integral role of rental vehicles in facilitating these journeys. Additionally, the shift toward remote work has enabled extended stays in vacation destinations, commonly referred to as workations, which require longer-term vehicle rentals. As per data from Destinations International, visitor bureaus have noted a significant increase in leisure-driven visitation, which directly translates to higher utilization rates for rental fleets. This sustained interest in domestic exploration ensures a steady baseline of demand, particularly during peak seasonal periods, thereby driving revenue growth for rental operators.

Business travel remains a cornerstone of growth for the U.S. car rental market due to the continuous need for corporate mobility and the economic activities that require physical presence. Despite the adoption of virtual communication tools, face-to-face interactions for negotiations, conferences, and client meetings remain indispensable for many industries. According to the Global Business Travel Association, U.S. business travel spending is expected to reach $381 Billion in 2024, showing consistent year-over-year growth and approaching pre-pandemic benchmarks. The Bureau of Labor Statistics indicates that there are over 130 million employed individuals in the U.S., a substantial portion of whom engage in travel related to their professional responsibilities. Major metropolitan areas and business hubs such as New York, Chicago, and San Francisco witness high concentrations of corporate renters who prioritize convenience, reliability, and premium vehicle options. The Society of Human Resource Management notes that employee mobility and relocation services also contribute to rental demand, as transient workers require temporary transportation during transition periods. Furthermore, the rise of the gig economy and freelance consulting has expanded the definition of business travelers, including independent professionals who rent vehicles for project-based assignments across different regions. As per the US Chamber of Commerce, small businesses constitute 99.9% of all US businesses, many of which rely on rental vehicles for logistics and client visits without maintaining large proprietary fleets. This diverse array of corporate users ensures a consistent demand stream that is less susceptible to seasonal fluctuations compared to leisure travel, providing rental companies with a stable revenue foundation throughout the year.

A significant restraint impacting the U.S. car rental market is the volatility in vehicle acquisition costs and the broader supply chain challenges that affect fleet management. Rental companies operate on thin margins and rely heavily on the ability to purchase vehicles at predictable prices and dispose of them at favorable residual values. According to Cox Automotive, the Manheim Used Vehicle Value Index decreased 8.2% year over year in mid-2024, which reflects substantial fluctuations that complicate financial planning and asset lifecycle management. When used car prices decline unexpectedly, rental companies face diminished returns on their capital investments, whereas high acquisition costs for new vehicles strain cash flows and limit fleet expansion capabilities. The Bureau of Labor Statistics reports that the producer price index for motor vehicles and parts has seen intermittent spikes, reflecting ongoing supply chain disruptions and inflationary pressures on manufacturing inputs. Additionally, the semiconductor shortage has left lasting impacts on inventory levels, forcing rental agencies to operate with older or less desirable vehicle models that may not meet evolving consumer expectations. As per the Federal Reserve, the federal funds rate was maintained at a range of 5.25% to 5.5% in early 2024, increasing the cost of financing for fleet purchases and squeezing operational budgets. These financial pressures compel rental companies to pass costs onto consumers through higher daily rates, which can dampen demand among price-sensitive segments.

The U.S. car rental market faces substantial restraints due to a complex and fragmented regulatory environment, coupled with escalating insurance liabilities. Unlike some other industries, car rental operations are subject to a myriad of state and local laws that govern taxation, liability, and consumer protection, creating a cumbersome compliance landscape. According to the Insurance Information Institute, commercial auto insurance net written premiums increased by 10% in recent annual reporting, with carriers increasing rates due to higher frequencies of severe accidents and increased repair costs. This surge in insurance expenses directly impacts the operational overhead of rental companies, forcing them to either absorb the costs or impose additional fees on renters, which can deter potential customers. Furthermore, various states have enacted specific legislation that limits the ability of rental companies to charge administrative fees or restricts certain contractual terms, thereby reducing revenue flexibility. The National Conference of State Legislatures highlights that differing regulations across jurisdictions require rental firms to maintain extensive legal and administrative resources to ensure compliance. Liability concerns are further exacerbated by the rising cost of litigation and settlements related to accidents involving rental vehicles. As per data from the National Highway Traffic Safety Administration, traffic fatalities increased by 10.5% in 2021 and have remained at a historically high level,s and this is leading to heightened scrutiny and potential legal exposure for rental agencies.

The transition toward electrification presents a significant opportunity for the U.S. car rental market. As environmental awareness grows, a segment of travelers actively seeks eco-friendly options, prompting rental companies to expand their electric vehicle offerings. According to the U.S. Department of Energy, the Clean Vehicle Credit provides a tax credit of up to $7,500 for the purchase of a new, qualified plug-in electric vehicle, which substantially lowers the total cost of ownership for rental fleets. Major rental operators have announced ambitious targets to electrify a substantial percentage of their fleets, capitalizing on these financial benefits while enhancing their brand image as sustainable entities. The Environmental Protection Agency notes that transportation is the largest source of greenhouse gas emissions in the U.S., creating strong policy momentum for electrification that supports infrastructure development. As charging networks expand, with the Federal Highway Administration overseeing the National Electric Vehicle Infrastructure Formula Program to provide $5 Billion for a national network of 500,000 chargers, the practicality of renting electric vehicles for long-distance travel improves markedly. This infrastructure growth alleviates range anxiety, a primary barrier to electric vehicle adoption. Furthermore, corporate clients with strict environmental, social, and governance mandates are increasingly preferring vendors that offer low-emission transportation options. As per the Sustainable Brands network, a growing number of Fortune 500 companies have committed to net zero emissions, driving demand for green business travel solutions.

The adoption of advanced digital technologies offers a profound opportunity for the U.S. car rental market to enhance operational efficiency and customer experience. The integration of artificial intelligence, machine learning, and mobile applications allows rental companies to streamline booking processes, optimize fleet distribution, and personalize service offerings. According to the Pew Research Center, 97% of Americans own a cellphone of some kind, and 90% own a smartphone, providing a ubiquitous platform for digital engagement and contactless rental experiences. Rental firms are leveraging this connectivity to implement keyless entry systems and digital check-in procedures, which reduce wait times and labor costs while appealing to tech-savvy consumers. The use of predictive analytics enables companies to anticipate demand surges in specific locations, allowing for more effective fleet allocation and reduced vehicle idle time. According to the International Data Corporation, global spending on digital transformation is projected to reach $3.9 Trillion by 2027, reflecting the industry’s commitment to innovation. Furthermore, telematics and Internet of Things devices provide real-time data on vehicle health and usage, facilitating proactive maintenance and extending asset lifecycles. This data-driven approach minimizes downtime and ensures that vehicles are always in optimal condition for renters. Additionally, digital platforms enable dynamic pricing strategies that adjust rates in real time based on supply and demand conditions, maximizing revenue per available vehicle.

The U.S. car rental market confronts a notable challenge in the form of labor shortages and difficulties in workforce retention, which directly impact service quality and operational capacity. The hospitality and transportation sectors have experienced significant turnover rates, exacerbated by shifting labor market dynamics and changing employee expectations post-pandemic. According to the Bureau of Labor Statistics, the quit rate in the accommodation and food services sector reached 4.1% in early 2024, indicating a volatile workforce environment that complicates staffing stability. Car rental operations rely heavily on frontline staff for vehicle preparation, customer service, and logistics, and insufficient staffing levels can lead to longer wait times, reduced vehicle cleanliness, and overall diminished customer satisfaction. The National Restaurant Association, which often tracks broader hospitality trends, notes that wage pressures have intensified as businesses compete for a limited pool of workers, forcing rental companies to increase compensation packages and invest more in training programs. These increased labor costs squeeze profit margins, particularly for smaller operators who lack the economies of scale enjoyed by major national brands. Furthermore, the seasonal nature of travel demand creates fluctuations in staffing requirements, making it difficult to maintain a consistent and experienced workforce throughout the year. As per the Society for Human Resource Management, 66% of organizations are experiencing a shortage of workers with the necessary skills, with the transportation industry facing unique difficulties due to the physical demands and irregular hours associated with rental operations.

Infrastructure limitations and urban congestion are another key challenge to the U.S. car rental market. As urban populations grow, traffic congestion has intensified, leading to longer travel times and increased wear and tear on rental vehicles. According to the INRIX Global Traffic Scorecard, the average American driver lost 42 hours to traffic congestion in 2023, which increases operational costs for rental companies through higher fuel consumption and maintenance needs. Furthermore, the availability of parking spaces in city centers and near popular tourist attractions is often limited and expensive, creating logistical hurdles for customers who must navigate complex parking regulations and fees. The American Planning Association highlights that many urban areas are prioritizing public transit and pedestrian zones over private vehicle access, which can discourage the use of rental cars in these environments. Additionally, the infrastructure for supporting large rental fleets, such as dedicated lot space at airports and city locations, is becoming increasingly scarce and costly due to real estate pressure. As per the Airports Council International, airport land use constraints are forcing rental car facilities to move further away from terminals, requiring shuttle services that add time and inconvenience to the customer experience.

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

4.75%

Segments Covered

By Application, Vehicle Type, Rental Duration, Service Model, And Region

Various Analyses Covered

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado.

Market Leaders Profiled

Enterprise Holdings, Hertz Global Holdings, Avis Budget Group, Sixt SE, Dollar Thrifty Automotive Group, Alamo Rent A Car, National Car Rental, Budget Rent a Car, Payless Car Rental, Fox Rent A Car

The leisure and tourism segment commanded the highest share of the U.S. car rental market in 2025 due to the robust recovery and expansion of domestic vacation travel. This dominance is underpinned by a cultural shift toward experiential travel, where personal mobility is essential for accessing diverse geographic locations. According to the US Travel Association, domestic leisure travel accounted for 73% of all domestic trips in recent years, demonstrating a clear preference for independent exploration over packaged tours. The National Park Service recorded approximately 325 million recreation visits annually, a metric that strongly correlates with high vehicle rental demand, as many of these natural destinations lack comprehensive public transportation infrastructure. Furthermore, according to the American Automobile Association, road trips remain the most popular form of vacation, with 82% of families planning one in 2024, reinforcing the necessity of rental vehicles for long-distance leisure trips. The rise of remote work has also facilitated the trend of extended stays or workations, where travelers combine leisure with professional duties in scenic locations. As per data from Destinations International, visitor spending in leisure-focused markets has surpassed pre-pandemic levels, indicating strong consumer confidence and willingness to spend on travel-related services, including vehicle rentals.

However, the business and corporate segment is a promising segment and is estimated to register a CAGR of 7.2% during the forecast period, owing to the resurgence of face-to-face corporate interactions and the expansion of the gig economy. While virtual communication tools remain prevalent, the need for physical presence in high-stakes negotiations, client meetings, and industry conferences has renewed demand for reliable corporate mobility solutions. According to the Global Business Travel Association, U.S. business travel spending is forecast to rise 11.5% in 2024 to $381 Billion, fueled by pent-up demand and the critical nature of in-person relationship building. The Bureau of Labor Statistics indicates that the professional and business services sector continues to add jobs, expanding the pool of professionals who require travel for work. Additionally, the rise of independent contractors and freelance consultants has broadened the definition of business travelers. According to the Upwork Freelance Forward 2023 study, 38% of the U.S. workforce performed freelance work in the past year, many of whom require flexible transportation options for project-based assignments across different cities. Unlike traditional employees who may have dedicated company cars, these independent professionals rely heavily on short-term rentals. Furthermore, companies are increasingly adopting blended travel policies that allow employees to extend business trips for leisure, known as bleisure, which increases the duration and frequency of rentals.

The economy and budget cars segment occupied the major share of the U.S. car rental market in 2025 due to their affordability and suitability for a wide range of consumer needs. This segment dominates because price sensitivity remains a key factor for both leisure and business travelers, particularly in an economic environment characterized by inflationary pressures. According to the Bureau of Labor Statistics, the Consumer Price Index for all urban consumers increased 3.4% over the 12 months ending April 2024, prompting consumers to seek cost-effective transportation alternatives. Economy vehicles offer lower daily rental rates and better fuel efficiency, making them an attractive option for budget-conscious travelers. According to the American Automobile Association, the average cost of owning and operating a new vehicle in 2023 was $12,182, and the superior mileage of compact and economy cars helps mitigate these costs for renters. Furthermore, the sheer volume of domestic air travelers, as reported by the Bureau of Transportation Statistics, creates a massive base of customers who require basic transportation from airports to their final destinations. Small businesses and solo corporate travelers also prefer economy cars for short-term assignments to minimize travel expenses. As per the National Small Business Association, 73% of small business owners identified the cost of goods and services as a significant challenge, driving the preference for economical rental options.

On the other hand, the premium and luxury vehicle segment is experiencing the fastest growth and is estimated to register a promising CAGR of 8.4% during the forecast period, owing to the rising disposable incomes and the desire for enhanced travel experiences. Affluent consumers are increasingly viewing car rentals not just as a utility but as part of the overall luxury travel experience, opting for high-end brands that offer superior comfort, performance, and status. According to the Federal Reserve, U.S. household net worth reached a record $156.2 Trillion in late 2023, enabling greater spending on discretionary items such as premium travel services. The Luxury Institute reports that high-net-worth individuals are prioritizing experiential luxury, where the quality of transportation significantly impacts their satisfaction with a trip. Additionally, corporate executives and high-level professionals often require premium vehicles for client impressions and personal comfort during business travel. According to the Global Business Travel Association, 71% of travel buyers expect their employees to travel more in 2024, with spending on premium class travel services recovering faster than economy segments. The availability of luxury electric vehicles also contributes to this growth, as tech-savvy affluent renters seek to experience the latest automotive innovations. Rental companies are expanding their luxury fleets to capture this lucrative market, offering models from brands like Tesla, BMW, and Mercedes-Benz.

The short-term rentals segment dominated the market by holding the largest share of the U.S. market in 2025 due to the nature of most business trips and weekend leisure getaways, which generally span a few days. According to the Bureau of Transportation Statistics, approximately 88% of all business trips in the U.S. are taken by personal vehicle or rental car and typically last less than a week. Similarly, the US Travel Association indicates that a significant majority of leisure trips are short-duration escapes, such as long weekend visits to nearby cities or national parks. The convenience of short-term rentals appeals to travelers who do not wish to commit to long-term leases or deal with the complexities of vehicle ownership for brief periods. Airport locations, which handle the bulk of rental transactions, primarily serve passengers arriving for short stays. As per Airports Council International data, the vast majority of air travelers are on trips lasting less than a week, creating a consistent and high-volume demand for short-term vehicle access. Furthermore, the flexibility of short-term rentals allows consumers to adjust their plans without long-term financial commitments, making it an ideal solution for uncertain travel schedules.

On the other hand, the long-term rental segment is estimated to register a CAGR of 8.8% during the forecast period in the U.S. market, owing to the normalization of remote work and the increasing number of individuals undergoing life transitions such as relocation or vehicle repair. According to the Pew Research Center, 35% of U.S. workers with jobs that can be done remotely are working from home all the time, enabling employees to live in different locations for extended periods. This flexibility has spurred demand for monthly car rentals that offer lower daily rates compared to short-term options. Additionally, the supply chain challenges in the automotive industry have led to delays in new vehicle deliveries, forcing consumers to rely on long-term rentals as a temporary substitute for car ownership. According to Cox Automotive, new vehicle inventory levels reached a 2-year high of 2.74 million units in early 2024, but specific model availability remains tight, prompting buyers to use rental services while waiting for their purchases. Insurance replacement rentals following accidents also contribute to this growth, as repair times for modern vehicles have increased. The National Highway Traffic Safety Administration notes that vehicle complexity has risen, leading to longer repair cycles.

The traditional corporate fleets segment held the major share of the U.S. car rental market in 2025 due to its extensive infrastructure, brand recognition, and ability to serve large-scale corporate contracts and airport-based demand. According to the Bureau of Transportation Statistics, airport locations account for approximately 50% of total rental revenue, and traditional operators hold exclusive or preferred agreements at most major US airports. These companies offer standardized services, loyalty programs, and a wide variety of vehicle choices that appeal to both business and leisure travelers. The reliability and consistency of traditional fleets are critical for corporate clients who require guaranteed vehicle availability and streamlined billing processes. According to the Global Business Travel Association, 62% of travel managers report that their companies have a formal travel policy that includes preferred rental car providers. Furthermore, traditional operators have invested heavily in digital technologies to enhance customer experience, including mobile apps for check-in and keyless entry, which helps them retain market share against newer entrants. Their ability to leverage economies of scale in vehicle procurement and maintenance allows them to offer competitive pricing while maintaining service quality.

However, the peer-to-peer car sharing platforms segment is the fastest growing segment in the service model category and is anticipated to showcase a CAGR of 13.2% during the forecast period, owing to the changing consumer preferences for unique vehicle options, cost effectiveness, and the convenience of neighborhood-based pickups. According to a report by the University of California, Berkeley’s Transportation Sustainability Research Center, the number of carsharing members in North America has grown significantly as consumers seek alternatives to traditional ownership. Peer-to-peer platforms allow individuals to rent out their personal vehicles, offering a diverse range of cars, including vintage, luxury, and specialized vehicles that are not typically available in traditional fleets. This variety appeals to enthusiasts and travelers looking for specific driving experiences. The lower overhead costs of peer-to-peer models often result in more competitive pricing, attracting budget-conscious consumers. According to the Sharing Economy Report, 68% of consumers are willing to share or rent personal items for insurance-backed profit. Additionally, the decentralization of rental locations allows users to pick up vehicles closer to their homes or destinations, avoiding the hassle of airport shuttles.

The U.S. is expected to demonstrate robust economic performance and continued dominance in the regional transportation sector for the next few years as it leverages its massive highway network and recovering travel demand. The U.S. stands as the singular and dominant entity in the North American car rental landscape due to the mature infrastructure, high vehicle ownership rates, and a robust tourism industry that drives consistent demand. A primary driving factor is the extensive highway system and urban sprawl that make personal vehicles a necessity rather than a luxury. According to the Federal Highway Administration, the U.S. has over 4 million miles of public roads, facilitating extensive road travel and necessitating reliable vehicle access for both residents and visitors. Another critical factor is the strength of the domestic aviation sector, which feeds directly into the rental market. According to the Bureau of Transportation Statistics, U.S. airlines carried 935 million passengers in 2023, representing a significant increase and supporting the high volume of airport-based rentals.

The competition in the U.S. car rental market is intense and characterized by the dominance of three major holding companies that control a significant portion of the industry. These established players leverage extensive fleets, broad geographic coverage, and strong brand recognition to maintain their leadership positions. However, the market is witnessing increased pressure from emerging peer-to-peer platforms and ride-sharing services that offer alternative mobility solutions. This shift forces traditional operators to innovate continuously by adopting digital technologies and expanding their electric vehicle offerings. Price competition remains fierce, particularly during peak travel seasons when demand surges, and inventory becomes scarce. Companies differentiate themselves through loyalty programs, customer service quality, and specialized vehicle selections. The barrier to entry remains high due to substantial capital requirements for fleet acquisition and infrastructure development. Nevertheless, niche players and regional operators find opportunities by targeting specific segments such as luxury rentals or long-term leases. The competitive landscape is further shaped by regulatory changes and economic fluctuations that impact consumer spending and operational costs. Adaptability and technological integration are crucial for sustaining market presence in this dynamic environment.

A few major players of the U.S. car rental market include

Key players in the U.S. car rental market primarily focus on fleet electrification to align with sustainability goals and regulatory pressures. Companies are increasingly integrating electric vehicles into their portfolios to attract environmentally conscious consumers and reduce carbon footprints. Digital transformation remains another critical strategy as firms invest in mobile applications and artificial intelligence to streamline booking processes and enhance customer experiences. Contactless technologies such as keyless entry and remote check-in are widely adopted to improve convenience and safety. Strategic partnerships with airlines, hotels, and ride-sharing platforms help expand market reach and create integrated travel ecosystems. Additionally, operators emphasize dynamic pricing models powered by data analytics to optimize revenue management based on real-time demand fluctuations. Fleet optimization through predictive maintenance and efficient allocation ensures high utilization rates and reduced operational costs. These combined strategies enable companies to maintain competitiveness and adapt to evolving consumer preferences in the modern transportation sector.

This research report on the US car rental market has been segmented and sub-segmented based on application, vehicle type, rental duration, service model & region.

By Application

By Vehicle Type

By Rental Duration

By Service Model

By Region

Please wait. . . . Your request is being processed

Frequently Asked Questions

The growth is driven by increasing tourism, business travel, airport transportation demand, and rising preference for temporary mobility solutions.

Major companies include Enterprise Holdings, Hertz Global Holdings, Avis Budget Group, and Sixt SE.

Economy cars, SUVs, luxury vehicles, vans, and electric vehicles are commonly rented.

Major metropolitan cities and tourist destinations such as California, Florida, Texas, and New York have high demand.

Mobile apps, online booking platforms, contactless rentals, GPS tracking, and AI-based fleet management are improving customer experience.

Increasing domestic and international tourism significantly boosts airport and leisure car rental demand.

High vehicle maintenance costs, fluctuating fuel prices, and fleet shortages are major challenges.

Ride-sharing platforms create competition, but car rentals remain preferred for long-distance and multi-day travel.

Fleet electrification, digital booking systems, autonomous vehicle integration, and flexible rental plans are key trends.

The market is expected to grow steadily due to increasing travel activity, technological advancements, and expanding mobility services.

Related Reports

Europe Car Rental Market Report

Jun 2024

Download Sample

Car Rental Market

Jun 2024

Download Sample

Shared Vehicles Market

Jun 2024

Download Sample

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com

Reports By Region

Reports By Industry

Please enter email

You are Subscribed

© 2026 Market Data Forecast All Rights Reserved.

© 2026 Market Data Forecast All Rights Reserved.